Have questions about your credit report? Review your free credit reports with a certified credit counselor! Knowing how to read your credit report is an important factor in taking control of your finances. The first step is to request your free credit report file, and to make it easier for you, we have created a step-by-step tutorial on how to obtain your free annual credit report.

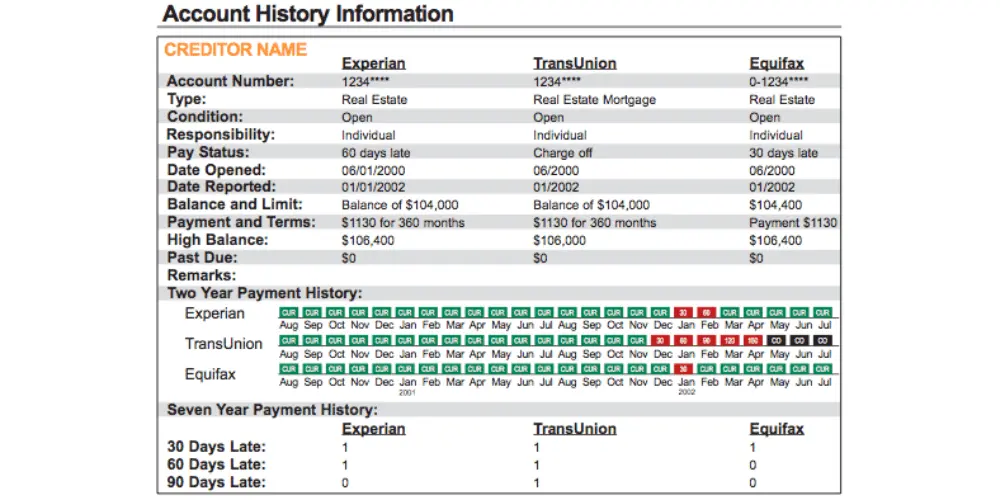

Let’s begin with the account history section, which may not be the first thing you’ll see when you open your free credit report, but it is the most important. It’s usually the largest section of the credit report. When calculating your credit score, FICO gives more weight to your payment history than any other category; it’s responsible for 35% of your credit score.

When looking at your credit report’s account history section, you’ll see a summary of each of your credit reports, including accounts that have been closed. Accounts are usually divided into five categories—Real Estate, Revolving, Installment, Other, and Collection. They may be separated into different sections depending on whether they have a negative or a positive impact on your credit file, whether the accounts are in collection, or other factors.

Key Information in Account History

For each account, you’ll find the following information:

Reviewing these details helps you verify the accuracy of your credit report. It’s vital to make sure that all information, including account types, balances, and payment histories, are correct. Inaccurate information can negatively impact your credit history.

Analyzing your payment history is key to understanding your financial habits. Late payments and their frequency can significantly affect your credit reports. This section should be checked thoroughly to identify any patterns of late payments and their impact on your credit reports.

Addressing any negative information in your payment history is critical. This might include late payments or high balances. Developing a plan to rectify these issues is essential for improving your credit score and overall credit reports. If you spot errors, promptly contact the credit bureaus to dispute them to fix mistakes.

Additional Considerations For Credit Scores and Credit Reports

It's not uncommon to find discrepancies in your free credit reports. Identifying and rectifying these discrepancies is crucial for maintaining a healthy credit score. Regular review of your credit report can help catch these errors early and improve your credit score.

Understanding your credit report is the first step in improving your financial situation. If anything in your credit report sections appears to be incorrect, you can write a letter to the credit bureaus requesting they correct any errors. See our free Consumer Guide to Good Credit for complete instructions on disputing out-of-date or inaccurate items on your credit report.

Reading and understanding your annual credit report, particularly the account history section, is key to managing your credit file and financial health. It highlights both the strengths and weaknesses of your credit history, offering insights into your financial behavior and its impact on your credit score. Check your credit score, carefully, identify wrong information, and tackle negative items, so you can enhance your financial health and creditworthiness. Remember, an accurate and well-managed credit report is your gateway to new credit, better interest rates, how many loans you qualify for, and stability.

Note: The visual format of your credit report file will differ depending on the credit reporting bureau that you ask for your report from. To make it easier to understand the differences, you may visit the following credit agencies: Equifax, Experian, and Transunion.