What’s a Good Credit Score?

Credit Score Ranges Explained

What is a credit score, and what’s considered a good credit score? If you’ve ever attempted to purchase a big-ticket item, such as a house or a car, the financing company likely spoke to you about your credit score.

This is one of the most defining factors lenders consider to determine whether or not to give you a loan.

Credit card companies and lenders use credit scores as one of the factors to determine loan amounts and interest rates. Your credit score is based on your credit report and can have a huge effect on just how much you end up paying. If you live in a state that allows auto and/or home insurance companies to consider your credit standing, improving your credit can help you lower your rates. The states of CA, HI, MD, MA, MI, OR, UT have restrictions – to learn more, visit this link.

What is a good score range?

Credit Score Ranges

Scores range from 300 to 850. Both FICO® score ranges and VantageScore ranges use 300 to 850, although VantageScore uses a range of 501 to 990.

What is the Average Credit Score?

National Score Averages

In the United States, the average FICO Score is 711 and the average VantageScore is 688.

Generally, a 680 score or above is considered a good score, while any score above 740 is considered excellent. But what is generally considered an average score?

Every expert, credit bureau, and loan officer has a different opinion as to where the threshold between good and poor credit. One loan agency may consider your score bad, but acceptable by another.

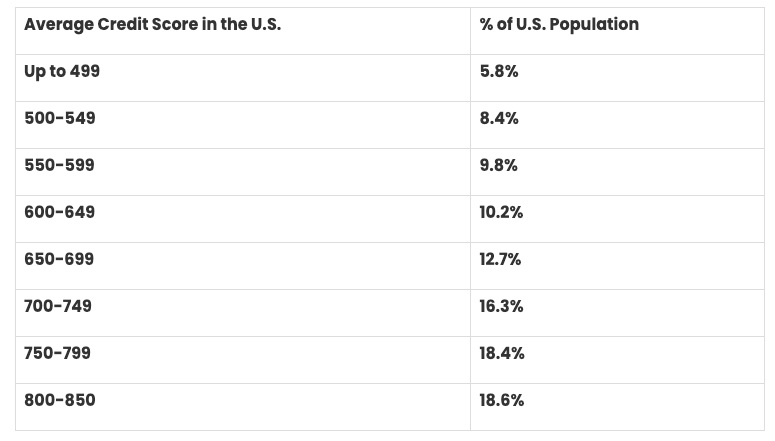

Furthermore, “good” is a relative term. Does “good” mean excellent or good enough? You can start by comparing your score to national averages. According to Fair Issac Corporation (FICO), first introduced in 1989, the following proportions of consumers have scores in the following ranges:

Based on this information, more than 50% of the population has a credit score of over 700, with 42% scoring below that level.

FICO is not the only scoring model used in the credit industry. There are different types of credit scores. The other main scoring model used is called VantageScore,® now in its third version, and which is called VantageScore 3.0.

What is a Bad Credit Score Range?

Impact of Low Scores

Bad credit score = 300 – 549: It is generally accepted that credit scores below 550 are going to result in a rejection of credit every time. If your credit scores have fallen into this range, improving your score is going to take some work.

Filing for bankruptcy can bring a score down to this level. Statistically, borrowers with scores in the low range are delinquent almost 75% of the time. If you continue to make your payments on time, your score should improve. There are certain types of loans, like home loans, that are hard to get with a score in this range, but there are still options for getting a mortgage with bad credit.

What is a Poor Credit Score range?

Challenges of Poor Scores

Poor credit score = 550 – 619: Credit agencies consider consumers with credit delinquencies, account rejections, and little credit history as subprime borrowers due to their high credit risk. Although it is possible to qualify for credit, it is often at very disadvantageous terms you will pay a much higher interest rate and penalty fees.

If you find your credit scores in this range, you should begin to address any specific credit problems you have to try to boost your score before applying for credit. Subprime borrowers typically become delinquent 50% of the time.

What is a Fair Credit Score range?

Benefits of Fair Scores

Fair credit score = 620- 679: Individuals with scores over 620 are considered less risky and are even more likely to be approved for credit.

In the mid-600s range, consumers become prime borrowers. This means they may qualify for higher loan amounts, higher credit limits, lower down payments, and better negotiating power with loan and credit card terms. Only 15-30% of borrowers in this range become delinquent.

What is a Good Credit Score range?

Advantages of Good Scores

Good credit score = 680 – 739: Credit scores around 700 are considered the threshold for “good” credit. Lenders are comfortable with this FICO score range, and the decision to extend credit is much easier. Borrowers in this range will almost always be approved for a loan and will be offered lower interest rates. If you have a 680 credit score and it’s moving up, you’re definitely on the right track.

According to FICO, the median credit score in the U.S. is in this range, at 723. Borrowers with this “good” score are only delinquent 5% of the time.

What is an Excellent Credit Score range?

Perks of Excellent Scores

Excellent credit score = 740 – 850: Anything in the mid-700, and higher is considered excellent credit and will be greeted by easy credit approvals and the very best interest rates. Consumers with excellent credit scores have a delinquency rate of around 2%.

In this high-end of credit scoring, extra points don’t improve your loan terms much. Most lenders would consider a credit score of 760 the same as 800. However, having a higher score can serve as a buffer if negative occurrences in your report. For example, if you max out a credit card (resulting in a 30-50 point reduction), the resulting damage won’t push you down into a lower tier.

What Affects a Credit Score?

Factors That Influence Your Score

While every credit scoring model is different, there are several common factors that affect your score. These factors include:

- Payment history

- Using your credit limits

- Balances on your active credit

- Credit inquiries

- Available credit

- Number of accounts

Each factor has its own value in a credit score. If you want to keep your number at the higher end of the credit score scale, it’s important to stay on top of paying your bills, using your approved credit, and limiting inquiries.

However, if you are in the market to purchase a house or loan, there is an annual 45-day grace period in which all credit inquiries are considered one cumulative inquiry. In other words, if you go to two or three lenders within a 45-day period to get to find the best rate and terms available for a loan, this only counts as one inquiry. This means that they are not all counted against you and will not affect your credit score.

Why Are My Credit Scores Low?

Understanding Score Drops

Lower credit scores aren’t always the result of late payments, bankruptcy, or other negative notations on a consumer’s credit file. Having little to no credit history can also result in a low score.

This can happen even if you have established credit in the past – if your credit report shows no activity for a long stretch of time, items may ‘fall off’ your report. Credit scores must have some type of activity as noted by a creditor within the past six months. If a creditor stops updating an old account that you don’t use, it will disappear from your credit report and leave FICO and or VantageScore with too little information to calculate a score.

Similarly, consumers new to credit must be aware that they will have no established credit report for FICO or VantageScore to appraise, resulting in a low score. Despite not making any mistakes, you are still considered a risky borrower because the credit bureaus don’t know enough about you.

How to Improve Your Credit Score:

Strategies for Score Improvement

Another common question when dealing with credit scores is “What can I do to improve my score?” There are many ways to improve your credit score to the higher end of the scale. Some of these methods include:

- Cleaning up your credit report

- Paying down your balance

- Paying twice a month

- Increasing your credit limit

- Opening a new account

- Negotiating outstanding balance

- Making payments on time

Credit.org offers consumers help in managing multiple payments. With a Debt Management Plan, you have the possibility of joining these payments into one lump sum at a lower interest rate. Learn more by reaching out to one of our credit counselors today!

The Takeaway

Navigating Credit Score Challenges

Of course, different lenders have different standards and your experience may vary. You may have a high credit score, but a negative public record on your credit file may hurt your chances of getting a loan. While credit scores don’t take your income into account, lenders will. No matter how good your credit score is, a lender will not approve you if they feel there are risks, such as your inability to repay.

No matter where you land on the scale, always remember that there are many factors that can both harm your credit history and help you improve your score. If you’re struggling with overcoming credit card debt, reach out to one of our trained credit counselors to help you pay off your debt faster and improve your personal financial situation.